Learn about our Making Work Supports Work project.

The recession has wreaked havoc on America’s workforce, putting pressure on states to make difficult budgetary choices. As the perennial concern of balancing the budget takes hold of state government, recessionary spending cuts further jeopardize the health and economic security of families. An increasing number of Americans face a large gap between their resources and their expenses, and the safety net is splintering just when workers need it the most. Nowhere is this more evident than in Mississippi, where the unemployment rate in 2009 was 10 percent, significantly higher than the national unemployment rate. More troubling, however, is the precipitous rise in statewide child poverty rates since the start of the recession. In 2009, 30 percent of Mississippi’s children lived in poor families versus 28 percent in 2008.

In a sluggish economic environment, where costs are rising faster than wages, Mississippians struggle to cover basic needs, such as food, shelter, health care, and child care. For those who can find work, employment alone is not enough. The Family Resource simulator (see FRS box) shows that even with full-time employment, low-wage workers in Mississippi cannot cover the cost of basic necessities without the help of work supports, such as food stamps, EITC, public health insurance, and child care subsidies. However, for many Mississippians, these work supports do not adequately support families as they move towards economic security. One of the biggest challenges facing Mississippians is the limited public health care provisions for parents. Medicaid is restrictively low with eligibility levels at 46 percent of the Federal Poverty Level. Outside of Medicaid, Mississippi has no state health insurance program for parents. Moreover, the continual decline of employer-sponsored health insurance and the prohibitive costs of private health insurance have led many Mississippians to forego health coverage altogether. More than 500,000 Mississippians went without health insurance in 2009. This situation has negative consequences not only for the health of parents, but for their family’s economic security and well-being. This brief uses results from the Family Resource Simulator to analyze Mississippi’s work support policies. It also identifies gaps in parental health insurance coverage and recommends policy reforms that could expand coverage among Mississippi’s working parents.

Tools for Policy Analysis

NCCP’s Family Resource Simulator is an innovative, web-based tool that calculates the impact of federal and state work supports on the budgets of low- to moderate-income families. The Simulator illustrates the effectiveness of current policies that reward and encourage work. NCCP also uses this tool to model potential policy reforms. Family Resource Simulators are available for 25 states, with more than 100 localities.

The Basic Needs Budget Calculator is a related tool that shows how much a family needs to make ends meet without the help of work supports. Users can select different household scenarios, and the Calculator adjusts the family’s tax liability and budget. Budgets are provided for nearly 100 localities across 19 states.

Making Ends Meet in Mississippi: Addressing the Earnings Gap

Research consistently shows that it takes far more than poverty-level wages to make ends meet in America. In order to cover the bare minimum of expenses – adequate food, stable housing, health care, and work-related expenses such as child care and transportation – families need incomes that are at least twice the Federal Poverty Level (or 200 percent FPL). In Mississippi, low-wage workers face a similar situation. Costs are rising faster than incomes, and hard-working Mississippians are left with budgetary deficits that can lead to persistent debt.

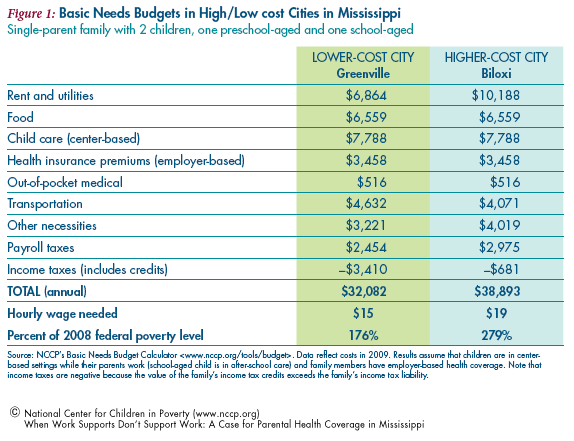

In Biloxi, for example, a single-parent family of three needs $38,893 to make ends meet (see Figure 1). This is more than 200 percent of the poverty level and equivalent to a full-time job at $19 an hour. Even in a low-cost city, such as Greenville, the same family must make $32,082 – or $15 an hour – to make ends meet. Thus, low-income Mississippians must earn significantly more than the minimum wage in order to fill the gap between their earnings and the cost of living. Health care and child care costs are prohibitively high across counties, accounting for a large portion of a family’s expenses and potentially leading to large budget deficits.

It is also important to note that this budget does not take into account other financial safeguards, such as education costs, savings for a home, or retirement. Nor does it include money for leisure activities or enrichment activities for children that could help in their socio-emotional development. And, finally, it does not consider any debt attached to medical expenses. However, the bottom line remains the same: workers face impossible choices that mean large opportunity costs for themselves and their families. Should parents seek center-based care for their children? Should they forego health insurance and hope they do not get sick? To this question, we respond later with potential policy reforms that could strengthen family health and income.

Work Supports Can Make a Difference

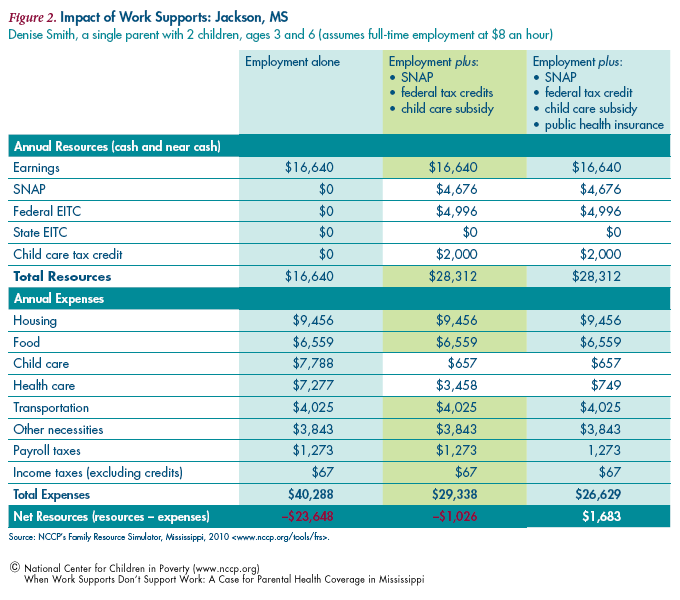

For workers who earn low wages, there are a number of federal and state work supports that can help close the gap between their earnings and expenses. These benefits include child care assistance, federal and state tax credits, food stamps, and public health insurance. For a detailed summary of work supports considered in this report, see NCCP’s publication, “Making Work Supports Work.” The bundle of work supports that a family receives can help them make ends meet. Consider the case of Denise Smith. Denise is a single mother with two children who lives in Jackson, MS. She works full-time at $8 an hour. Without work supports, her family faces a gap of nearly $24,000 between her earnings and the cost of basic necessities (Figure 2, first column). But as benefits– including federal and state tax credits, food stamps, child care assistance and public health insurance – are added to her budget, Denise gradually increases her resources until she is able to cover her family’s basic expenses (Figure 2, last column). And her net resources (resources minus expenses) allows her to start saving or paying down debt. In this case, Denise has $1,683 to put towards her family’s future. Figure 2 also shows the significant impact that public health insurance can have on families who are eligible to receive it. On the expense-side, we see that without children’s public health insurance, the Smith family faces a shortfall of over $1,000 annually, despite working full-time and receiving multiple benefits. In reality, when parents are working full-time at $8 an hour, they are already ineligible for Medicaid and are paying up to $3,442 (assuming private health coverage) and ($749 assuming employer health coverage). More often than not, parents choose to go without health insurance, leaving themselves vulnerable to medical emergencies that can lead to debt.

When Work Supports Fail to Support Work

As we have seen, work supports can make a tremendous difference to a low-wage worker’s financial bottom line. Unfortunately, there are many potential barriers to participation and, therefore, too many workers do not receive all the benefits for which they are financially eligible. Such barriers include inadequate state funding, lack of information, lengthy and cumbersome application procedures, and the stigma associated with seeking public assistance.

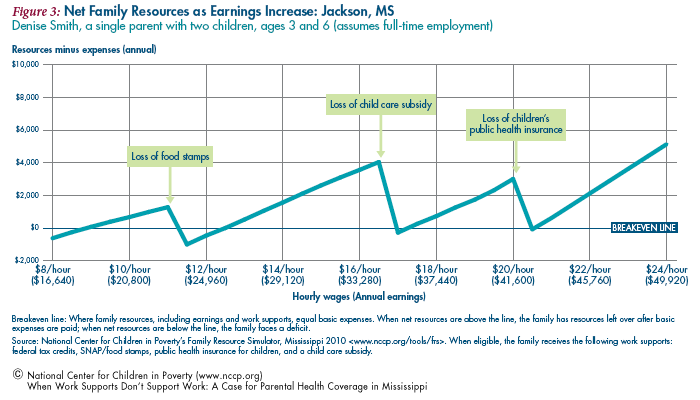

Moreover, work supports are typically means-tested so as workers begin to ascend the career ladder and their earnings rise above the official poverty level, they begin to lose eligibility for critical benefits. In some cases, even a very small increase in income due to a promotion or an additional job can result in a substantial loss of benefits, known as benefit “cliffs.” These benefit cliffs can occur in rapid succession, leading families towards large financial losses. This particular pattern in the current work support system creates natural disincentives for families to progress in the workforce.

If we turn, again, to the example of Denise Smith, we notice that she is able to make ends meet with work supports and a full-time job at $8 an hour (see Figure 3). The analysis below assumes that Denise receives the full package of work supportstax credits, food stamps, public health insurance, and child care subsidies. As her wages rise and she progresses in the workforce, she faces multiple benefit cliffs that bring her below the breakeven line (the line represents the point at which the family’s resources cover basic expenses). The first benefit cliff occurs when her wages hit $10 an hour and she loses food stamps. When Denise loses food stamps, she experiences a budget shortfall of nearly $1,000. The second cliff occurs when the family loses child care subsides at $16 an hour. Even though Denise works hard to increase her earnings over time, the loss of child care puts her in a precarious financial situation. Child care costs are prohibitive and Denise must pay out of pocket for full-time centerbased care. Since it takes at least $16 an hour just to cover basic necessities in a moderate-cost city like Jackson, these work supports fail to support the Smith family in the long-term. In fact, it is not until her earnings exceed $21 an hour that further wage increases actually help Denise build savings. The cliffs trace a familiar narrative: as Denise climbs the career ladder, the rungs fall out from under her, preventing her from ever attaining financial footing and long-term economic security.

A Closer Look at Work Supports: When Health Insurance Fails to Support Parents

In the previous analysis, Denise has access to a variety of work supports, including health insurance. We can see the impact that child health insurance has on her budget, as a benefit cliff results from her wage increase at $20 an hour. However, what we don’t see in the analysis is the benefit cliff that occurs before Denise can attain full employment. At around $6,000/year (far below the earnings level of a full-time minimum wage worker), Denise loses her sole source of health insurance when she becomes ineligible for Medicaid. Unfortunately, Mississippi sets its income eligibility level for Medicaid below 50 percent of the poverty level. This makes it virtually impossible for parents in Mississippi to remain insured once they have full-time employment. They must choose to pay for employer-based coverage, private insurance, or risk going without health insurance. In this analysis, we assume that Denise receives private health insurance when she becomes ineligible for Medicaid, but in reality, most parents will not spend money where they don’t have it.

Across states, working parents face the challenge of inadequate parental health insurance. Of the 50 million uninsured in the U.S., 77 percent come from working families. Yet, only a third of states have public health insurance programs open to parents with incomes of up to at least 200 percent of the federal poverty level- the minimum level of income families need to get by. And the disparity between parents and children is increasing: the median eligibility level for child health insurance is 235 percent of FPL while the median for a working parent is 64 percent of FPL.

While health insurance for children has been a growing priority, parental health insurance remains limited at best. Among poor parents, 47 percent are uninsured, whereas 13 percent of poor children are uninsured. The disparity among health coverage for parents and children in Mississippi reveal the need for better access to parental insurance. Some states have already responded to the need with innovative health insurance initiatives that expand or reform public programs (see box). The financing mechanisms that support these state initiatives are equally as important as broad program access, as they can strengthen or undermine the program’s outcomes. The states that currently offer parental health insurance have funding streams that enable successful programs to function over the long-term (see box).

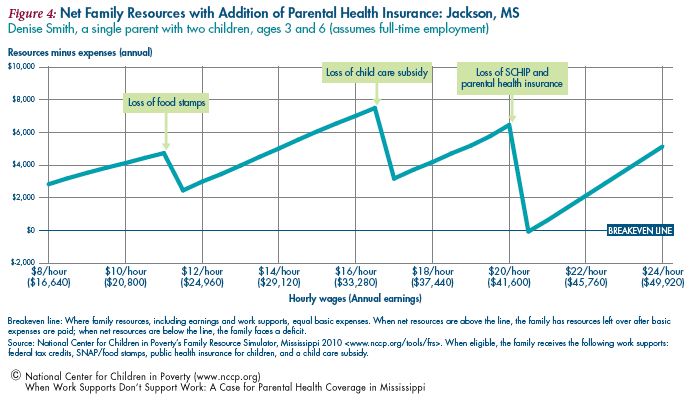

States can implement a range of policies and programs that can be effective in reducing the number of uninsured parents. States can apply for waivers to expand Medicaid and or/CHIP to higher-income parents, they can fund state programs directly by providing reduced-price coverage, and they can provide economic incentives for businesses to supply affordable, quality coverage. Mississippi should develop an expansion program model similar to Wisconsin that would cover parents at a higher income level. Figure 4 shows the effects of creating a parent expansion program that increases the eligibility threshold to 200 percent FPL. The benefit cliffs change to reflect the added health care subsidies which allow Denise to remain insured and well above the breakeven line as her wages increase. She now faces a health insurance benefit loss at the $41,000 wage level compared to less than $6,000 if she was on Medicaid. This cushion of resources makes a significant difference to Denise’s health and economic security. In fact, the difference is clearly illustrated with the loss of health insurance, which pulls Denise’s family below the breakeven line.

The present-day economic climate in Mississippi is a contributing factor to the rise of uninsured parents. It is, therefore, critical that Mississippi enact policies that increase access to health insurance, particularly to parents who would otherwise forgo the costs associated with private or employer-based coverage. The success of Massachusetts in sharply reducing the number of uninsured signals a promising approach to health insurance expansion. As our analysis shows, health care coverage enables a family to maximize its resources by reducing expenses while supporting families as they progress in the workforce. These findings are consistent with research that links health insurance to better parental health and more hours of work. These studies generally suggest that parents who experience chronic health conditions are more likely to work fewer hours and to receive lower wages than their counterparts, diminishing their ability to attain employer sponsored insurance coverage and to afford private coverage.

Increasing Parental Health Care Coverage through State-level Initiatives

Comprehensive Health Care Reform

Massachusetts – The first state to pass legislation in support of a comprehensive public health insurance program, Massachusetts enacted health care reforms in 2006 that expanded publicly subsidized coverage to nearly all state residents. The recent addition- Commonwealth Care targets uninsured adults earning at or below 300 percent of the Federal Poverty Level (FPL) who would not otherwise qualify for Medicaid. Recent job losses between 2008 and 2009 have led to an increase in Commonwealth Care enrollment by 16,000 enrollees. In 2008, the total number of uninsured in Massachusetts was only 2.6 percent of the state’s residents, which was the lowest rate in the country. Moreover, the decline in the number of uninsured residents accounts for 22 percent of the total drop in the national non-elderly uninsurance rate. While continued success will depend largely on cost containment as demand for coverage rises, Massachusetts still remains the harbinger of comprehensive state-wide health care reform.

Financing – Commonwealth Care is financed through a federal Medicaid waiver, which was renewed in September 2008.* The federal funding agreement provides flexibility while also limiting the state to the availability of federal dollars. Thus, while the renewal of this singular financing mechanism is essential to state health reform (it primarily funds the subsidies provided through the Commonwealth Care program), Massachusetts will likely struggle to balance spending with available resources in the aftermath of the Great Recession while federal funding levels continue to fluctuate.

Medicaid Program Expansion

Wisconsin – Enacted in 2007, BadgerCare Plus provides targeted expansions to increase benefits for underserved populations. Specifically, BadgerCare Plus augments existing state programs in one comprehensive program that expands coverage to children, parents and childless adults of various income levels. Parents with incomes below 150 percent FPL do not pay premiums and parents with incomes below 300 percent FPL pay premiums capped at five percent of family income. As of April, 2010, more than 86,500 additional parents were covered. Currently, 245,054 parents are covered through BadgerCare Plus, and the new provision for childless adults has led to an additional 60,614 participants. Even though BadgerCare Plus is relatively new, it has already provided coverage to a total of 770,000 state residents (235,000 more than before the start of the program). As post-recession fiscal pressures and growing demand for coverage weighs upon states, Wisconsin serves as an example of how expansions can be built into pre-existing state programs – like Medicaid – to streamline access to the uninsured.

Financing – BadgerCare Plus is financed through a combination of state revenue, federal matching funds for Medicaid/SCHIP, and premiums paid by enrollees. The childless adult expansion is primarily financed through the $60 application fee.

__________

*The MassHealth 1115 Waiver program is a Section 1115 “Medicaid Research and Demonstration” waiver- a federal provision which allows states to implement Medicaid policies that expand eligibility to underserved populations with matching federal funding. The MassHealth 1115 Waiver program, a “budget neutral ceiling” places a cap on the amount the state can spend while still receiving a federal reimbursement based on a projection of what the state would have spent- in federal dollars- if it had operated a traditional non-waiver Medicaid program.

Moreover, parents’ a8ccess to health care is a key predictor of access to health care for children. In fact, research suggests that when health insurance is extended to parents, enrollment and retention in child health insurance improve. Parents who forego health coverage may not access regular medical care which could affect their health or, in unforeseen medical emergencies, lead to financial insolvency. In recent years, health care costs have become a major source of debt and bankruptcy in the United States. Unfortunately, low-income parents are more likely to be uninsured and are also more likely to have chronic health problems than their counterparts. Finally, an illness or health condition can interfere with a parent’s ability to care for a child, thereby affecting the health and wellbeing of the family. A separate health insurance program for parents (as illustrated in Figure 4) will strengthen the healthy development and economic security of Mississippi’s families.

The Erosion of Employer-based Health Insurance

According to recent studies, roughly 58.9 percent of Americans under the age of 65 received health insurance through their employer compared to nearly 62 percent in 2008. This represents the ninth consecutive year that employer-based health insurance rates fell. While health care coverage fell in every state, Mississippi experienced one of the largest declines in employer-sponsored health insurance rates, falling from 60.4 percent in 2000 to 50.4 percent in 2009. Although no one has been spared from the decline of job-based insurance over the last decade, our analysis shows that low-income workers are the most vulnerable to changes in resources and expenses (see Figure 2). Therefore, declines in employer-sponsored insurance are most significant for those at the bottom quintile.

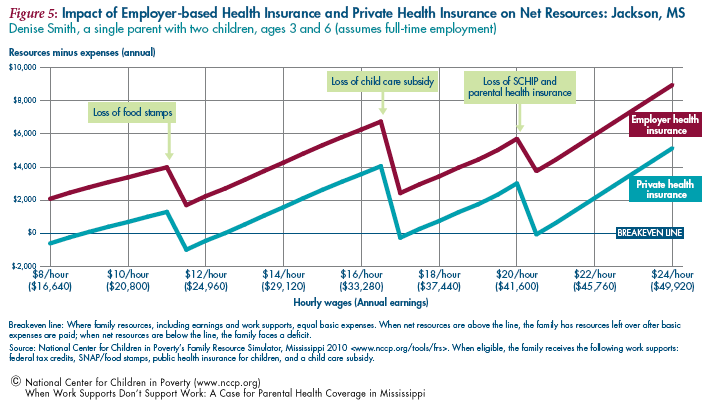

Generally, low-wage workers are less likely to obtain health insurance through their employers than higher-wage workers. And, a majority of workers in firms that do not offer insurance are low-wage earners. The disparity across the wage distribution is striking: only 39.8 percent of workers in the lowest quintile (making less than $9.38 an hour) had employer-based health insurance compared to 85 percent of those in the top quintile in 2009. For working parents, like Denise, who are cut off of Medicaid before they have the resources to pay for health insurance premiums, employer-sponsored health care is particularly crucial. Without it, families must pay prohibitive rates for private health insurance. Figure 5 illustrates the impacts of employerbased and private health insurance costs on the family’s ability to make ends meet. If Denise chooses to take employer-sponsored health insurance once she is at full-time employment, the expenses from premiums are significant but not enough to pull her below the breakeven line. However, if she is unable to get group health insurance rates through her employer (as is the case for an increasing number of low-income workers in small businesses or in seasonal jobs), Denise must buy coverage on the open market. Figure 5 shows the impact of additional private health insurance costs on the family’s bottom line. Even when Denise’s earnings double from $9 to $18 an hour, she still hovers below the breakeven line and cannot fill the gap between her resources and expenses until she earns over $21 an hour. In reality, Denise would likely forgo health insurance for the sake of maintaining her financial footing and pay out of pocket for medical expenses.

Employers can provide an affordable and direct path towards health care for the majority of workers. However, in Mississippi, small businesses often cannot afford to pay health benefits. The consistent erosion of job-based insurance suggests that employers are becoming increasingly less likely to offer insurance to their employees, especially during the recession. The cost of providing health insurance is particularly burdensome to small businesses. In 2008, employers with fewer than 10 workers paid $350 more for each employee’s health insurance, on average, than firms with 50 or more worker. In 2009, more than a quarter of small businesses (with less than 10 workers) did not offer health insurance coverage to their employees.

A healthy and productive workforce is vital to economic development. States should not only encourage businesses to provide quality health coverage, but they should make it an affordable option. The recent enactment of the Patient Protection and Affordable Care Act (PPACA) will support small businesses and workers through better health care access. Under the Act, tax credits offered on the basis of a sliding scale would alleviate costs to small business employers who could use the tax credits towards the purchase of health insurance for their workers. The maximum value of the credit in 2010 was 35 percent of the employer’s costs for employee coverage. More than 93 percent of the 36,600 small businesses in Mississippi were eligible to receive a tax credit last year, and 11,400 were eligible for the maximum tax credit. However, since there are no employer mandates for small businesses within the law, Mississippi should encourage eligible small businesses to apply for the tax credit and facilitate enrollment in the program so employers can maximize their resources. These small economic incentives can create significant opportunities for businesses to invest in a stronger, healthier workforce.

In summary, this analysis exposes a work support system in Mississippi that does not effectively support the health and economic well-being of its working families. Mississippi’s small businesses and low-income workers struggle under the weight of unaffordable health care coverage. Employers rely on a healthy and productive workforce, just as workers rely on quality benefits and work supports. Not only is it imperative for parents moving into the workforce system to have decent health coverage, it is also crucial that they don’t face trade-offs between their financial well-being and their health as their earnings increase.

While a dominant child-specific focus within the Medicaid expansion has led to an increase in child coverage, parental health insurance should not be left out of state policy reforms. The link between parents’ health and children’s health is, in itself, a strong argument for improving health care access among low-income parents. Mississippi, like other states, will benefit from PPACA, but immediate reforms should be implemented now in order to strengthen the workforce. As this study shows, states have already proposed and implemented innovative health care reforms that improve cost containment and increase insurance coverage. Mississippi should support similar reforms and facilitate access to affordable, quality health insurance for its many working parents.

Endnotes

1. Chau, Michelle. 2009. Low-income Children in the United States: National and State Trend Data (1998-2008). New York, NY: National Center for Children in Poverty, Columbia University, Mailman School of Public Health.

2. Mississippi Economic Policy Center. 2010. Fact Sheet. www.mepconline.org (accessed Dec. 16, 2010).

3. Dinan, Kinsey. 2009. Budgeting for Basic Needs: A Struggle for Working Families. New York, NY: National Center for Children in Poverty, Columbia University, Mailman School of Public Health.

4. Purmort, Jessica. 2010. Making Work Supports Work: A Picture of Low-wage Workers in America. New York, New York: National Center for Children in Poverty, Columbia University, Mailman School of Public Health.

5. Cauthen, Nancy. 2007. Improving Work Supports: Closing the Financial Gap Between Low-wage Workers and Their Families. New York, New York: National Center for Children in Poverty, Columbia University, Mailman School of Public Health.

6. All budget data are based on calculations derived from NCCP’s Basic Needs Budget Calculator.

7. We make the assumption that the family receives private health insurance. As we discuss later in the report, employers are increasingly less likely to provide group health insurance plans.

8. Five Facts About the Uninsured. 2010. Kaiser Commission on Medicaid and the Uninsured. www.kff.org (accessed Feb. 1, 2011).

10. Lee, Chris; Palosky, Craig. 2010. States Sustain and Expand Coverage for Low-income Children and Families Despite Recession, But Gains are Threatened by Impending End of Federal Assistance. Kaiser Family Foundation.

11. Hadley, J. 2003. Sicker and Poorer- The Consequences of Being Uninsured: A Review of the Research on the Relationship Between Health Insurance, Medical Care Use, Health, Work, and Income. Medical Care Research Review 60: 3S-75S.

13. Kaiser Commission on Medicaid and the Uninsuried. 2009. Massachusetts Health care Reform: Three Years Later. www.kff.org/uninsured/upload/7777-02.pdf (accessed Mar. 21, 2011).

15. CFED. 2010. Access to Health Insurance: 2009-2010 Assets and Opportunity Scorecard. http://scorecard.cfed.org (accessed Mar. 8, 2011).

Seifert, Robert W. 2008. Massachusetts Medicaid Policy Institute. The Basics of MassHealth: Fact Sheet. www.massmedicaid.org (accessed Apr. 7, 2010).

Sparer, Michael. 2003. Leading the Health Policy Orchestra: The Need for an Intergovernmental Partnership. Journal of Health Politics, Policy, and Law28: 2-3.

16. Leininger, Lindsey; Fridsam, Donna; Dague, Laura, et al. 2011. Wisconsin’s BadgerCare Plus Reform: Impact on Low-Income Families’ Enrollment and Retention in Public Coverage. Health Services Research 46(1): 336-347.

Witgert, Katherine E. 2009. BadgerCare Plus: Medicaid and Subsidies Under One Umbrella. National Academy for State Health Policy.

17. Kaiser Family Foundation. 2010. Wisconsin’s BadgerCare Plus Program: Moving Forward on Health Reform Amid a Recession. Kaiser Commission on Medicaid and the Uninsured.

18. Dinan, Kinsey Alden; Briggs, Jodie. 2009. Making Parents’ Health Care a Priority. New York, NY: National Center for Children in Poverty, Columbia University, Mailman School of Public Health.

19. Dubay, L; Kenney G. 2003. Expanding Public Health Insurance to Parents: Effects on Children’s Coverage Under Medicaid. Health Service Research 38(5): 1283-1302.

Aizer A; Grogger J. 2003. Parental Medicaid Expansions and Health Insurance Coverage. National Bureau of Economic Research. NBER Working Paper 9907.

Miller, Jane E; Gaboda, Dorothy; Nugent, Colleen N.; Simpson, Theresa M. 2011. Parental Eligibility and Enrollment in State Children’s Health Insurance Program: The Roles of Parental Health, Employment and Family Structure. American Journal of Public Health 101(2): 274-277.

Rosenbaum, Sara; Whittington, Ramona. 2007. Parental Health Insurance Coverage as Child Health Policy: Evidence from the Literature. The George Washington University Medical Center for First Focus.

20. Zelda, Cindy; Rukavina, Mark. 2007. Borrowing to Stay Healthy: How Credit Card Debt is Related to Medical Expenses. Demos.

22. Gould, Elise. 2010. Employer-sponsored Health Insurance Erosion Accelerates in the Recession: Public Safety Net Catches Kids but Fails to Adequately Insure Adults. EPI Briefing Papter. Economic Policy Institute.

25.Long, Stephen; Marquis, Susan. 1993. Gaps In Employer Coverage: Lack of Supply Or Lack of Demand? Health Affairs 12(1): 282-293.

28. Families USA and Small Business Majority. 2010. A Helping Hand For Small Businesses: Health Insurance Tax Credits. www.familiesusa.org/assets/pdfs/health-reform/Helping-Small- Businesses.pdf (accessed Feb. 4, 2011).